A couple of hours ago, IBM announced that they had entered into an agreement to acquire Red Hat for $34 billion in cash. That’s one of those big milestones in IT history that will have a profound impact for years to come. But is that totally surprising? Not quite...

At the beginning of the year, as part of my 2018 predictions, here is what I had posted on Twitter:

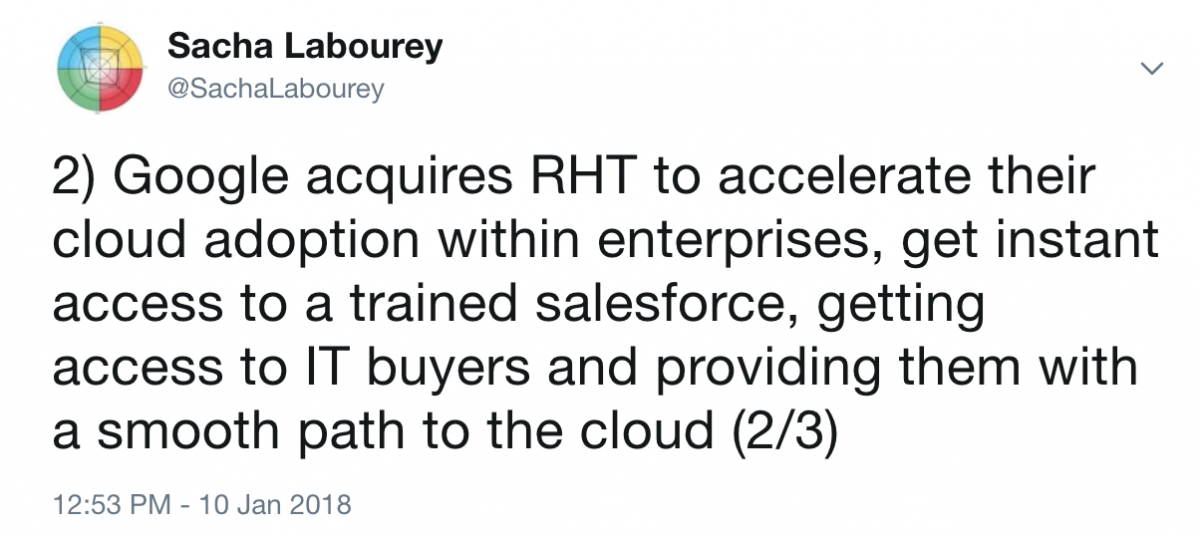

So I was only partially right. It wasn’t Google after all, it was IBM.

The inevitable outcome

This outcome was inevitable for two reasons:

- The first is that Red Hat owns amazing assets for this cloud era, has great developer love and also provides access to pretty much all CIOs on the planet. From the classic Red Hat Enterprise Linux (RHEL) and JBoss to the modern OpenShift (~Kubernetes) and Ansible, Red Hat owns key assets to provide enterprises a smooth ride from the current IT to the public cloud era. Public cloud vendors might operate the best destinations, but if there is no path to get there, it is not worth much. As such, Red Hat acts as a fantastic gateway to the public cloud.

- The second reason is less rosy. Red Hat has a unique business model crafted in the late 90’s/early 00’s when open source lived in a much stronger ideological environment. Red Hat has a pure open source business model, which means that *anything* they do is available in open source. Monetization, in the form of yearly recurring subscriptions, happens on top of those free assets. While this has made it possible for Red Hat to reach a venerable ~$3B in revenue, this is a “harder” business model as it can be hard to justify a big premium when all of your value is otherwise freely available. If you compare Red Hat’s growth to VMware for example, a comparable player in the infrastructure market, VMware reached about 3x Red Hat’s size in less time.

With the advent of the public cloud, pure open source models are very hard to defend. The massive cloud players (dominated by Microsoft, Amazon and Google under our longitudes), have reached such a critical mass that they are able to provide similar software infrastructure foundations to what Red Hat provides (frequently by simply “taking” software developed by Red Hat) but at a much-reduced cost. For those organizations, the objective is not so much to monetize those software assets, as to move compute workloads to their cloud. They want to be the next generation data center, not sell operating systems. This makes it a very hard competitive environment… Think about it: competitors are able to take your assets and make them available for free for the same customer base. As such, with limited future growth potential for its historical assets (RHEL and middleware) and a modern portfolio not yet able to carry the full weight of Red Hat and under increasing pricing pressure from cloud vendors, my bet was on a takeover of Red Hat in 2018.

A quick parenthesis on Red Hat’s business model. The above explains why, in the last few years, as discussions around open source monetization became less emotional, most open source-based companies have opted for an open core business model, mixing the open source benefits of wide-scale adoption to the proprietary software benefits of differentiation. Open core business models have become the norm since then and only two companies were left operating with a pure open source business model: Hortonworks and Red Hat. Both recently acquired…

In the cloud era, cloud vendors have massive scale and aren’t focused on monetizing software assets, this makes them a new shape of competition which, unless handled properly, make them highly lethal.

A surprising destination

The bottom line is that I’m not surprised by Red Hat being acquired. I am, however, much more surprised by who the acquirer is. This is a bold move by IBM, which might prove to be their best single bet to remain relevant for another few decades.

In this new cloud era, developer mindshare is as important as enterprise mindshare. Bottom-up meets top-down. Developers vote with their feet. In this subtle dance, successful public cloud vendors have been able to get their steps right. IBM on the other hand, while very strong in top-down motions, hasn’t been able to really build up developer love. The impact has led IBM to be in the second tier of cloud vendors, along with Oracle, after AWS, Microsoft and Google.

Consequently, through that acquisition, Red Hat will provide IBM with some much-needed developer’s love and a modern software portfolio. IBM could provide Red Hat with the means to be much more aggressive with their M&A strategy.

So, can this acquisition turn into something valuable for this new IBM? Yes, it can. If Red Hat is able to make IBM become relevant in the public cloud, this could be a game changer well worth the $34B…and if it doesn’t work, IBM will become much less valuable. The cloud is acting as an “all or nothing” forcing function for companies, where no room is left for small or even medium-sized vendors.

Public cloud acquisition costs are irrelevant today

Public cloud is becoming the new infrastructure. This is where, ultimately, all workloads will be running. This is a massive and hugely strategic market and a once-a-lifetime opportunity for a few vendors to become massive organizations. We are talking black hole-sized vendors. In that new era, there will be no room for “average-sized” vendors. We will face an oligopoly of a few massive vendors, with a tiny tail for the IT nostalgic.

My belief is that in the growing phase of such a market, the sales acquisition costs do NOT matter. For every $1 of business a vendor acquires today, the TCV (total contract value) associated to that $1 over the lifetime of that contract might be well beyond $1,000. In that phase, it is critical for vendors to seize the biggest market share today, at any cost.

As such, given IBM’s lag on the cloud market, spending $34B on Red Hat can make a lot of sense IF IBM is able to leverage this asset to increase their cloud market share to become one of the top three cloud vendors. That’s the bet they did and this is the bet they HAD to do. In some ways, this is IBM’s last chance to matter on that market and if they don’t, they’ll slowly become a big but less relevant player. This is an “all or nothing” bet. It is bold.

So why not Google?

My 2018 prediction was on Google acquiring RHT, not IBM. My logic was similar though. Despite amazing technology, Google is currently the number #3 cloud vendor and, as Microsoft will tell you from their experience in the mobile space, it is not great to be the #3 vendor, in any market…

But unlike IBM, Google does not need more cool technology or more developer love. What Google is missing is a true enterprise trait added to their DNA. To date, Google has tried building that trait on their own, but this has been only mildly successful. My view was that Google should acquire that trait. By acquiring Red Hat, Google would have had instant access to a worldwide enterprise salesforce with entry to all CIOs on the globe, and extreme data center credibility. Furthermore, Google and Red Hat product portfolios are amazingly similar. This would have been an instant boost for Google’s enterprise credibility and business, and if $1 of cloud business acquired today is truly worth $1,000 in the long run, even at a one-time $34B fee this is a bargain (Amazon AWS revenues are probably already at half this number per year). So, why didn’t it happen? My bet is that Google Cloud’s CEO, Diane Greene, is certainly aware of that and must be very frustrated to not be able to make much bolder moves. Why? In the grand scheme of self-driving cars and other grandiose projects, I’m not convinced that Google’s founders necessarily see the cloud as an absolute necessity worth spending $34B.

The cloud is having a transformational impact on the IT market. After transforming Amazon into “the new Amazon,” and transforming Microsoft into “the new Microsoft,” it will be on IBM to prove this acquisition can transform them into “the new IBM.”

At CloudBees, we are firm believers in that public cloud destination — so all of our software is now Kubernetes-native. Yet, we also understand this will be a journey and that enterprises need a path to get there. This is why our platform supports all customer use cases, from Go and Kubernetes to Java, .Net and mobile, from on-premise to public cloud, all under a single umbrella, a single pane of glass. As the market is moving towards that inevitable public cloud oligopoly, it is more important than ever for customers to be able to rely on a vendor that can independently orchestrate workloads to any destination. We are the Switzerland of software delivery. Anything less than this means you would be transforming this oligopoly into a monopoly.

Onward,

Sacha Labourey

CEO and co-founder

CloudBees

A native of Switzerland, Sacha graduated from EPFL in 1999. At EPFL, he started Cogito Informatique, an IT consulting business. In 2001, he joined Marc Fleury’s JBoss project as a core contributor, implementing JBoss’ original clustering features. He went on to become general manager for JBoss Europe, leading strategy and helping to recruit partners that fueled JBoss’ growth. In 2005, he became CTO, overseeing all of JBoss engineering. When Red Hat acquired JBoss in 2006, Sacha played a crucial role in integrating and productizing the JBoss software with Red Hat offerings. Sacha went on to become co-general manager of Red Hat’s middleware division. He left Red Hat in 2009 and founded CloudBees in March 2010. Follow Sacha on Twitter .

A native of Switzerland, Sacha graduated from EPFL in 1999. At EPFL, he started Cogito Informatique, an IT consulting business. In 2001, he joined Marc Fleury’s JBoss project as a core contributor, implementing JBoss’ original clustering features. He went on to become general manager for JBoss Europe, leading strategy and helping to recruit partners that fueled JBoss’ growth. In 2005, he became CTO, overseeing all of JBoss engineering. When Red Hat acquired JBoss in 2006, Sacha played a crucial role in integrating and productizing the JBoss software with Red Hat offerings. Sacha went on to become co-general manager of Red Hat’s middleware division. He left Red Hat in 2009 and founded CloudBees in March 2010. Follow Sacha on Twitter .